Life expectancy has increased significantly over the past couple of centuries. Science now predicts that you may live to be 100. With the progress in science and technology, it is likely the life expectancy trend will continue. This begs the question, will your money last that long? If not, how can you set up your finances so that it can? This article will look at:

- Calculating Your Life Expectancy

- Historical Life Expectancy Trends

- Future Lifestyle Design

- Forced & Unplanned Retirement

- How Much Do You Need To Save

- How To Make Your Money Last Indefinitley

Will You Live To Be 100?

I’m not suggesting this will happen in our lifetime. However, it is predicted that if you are currently 25 years of age and female, then you have a 24.5% chance of living until 100. You can use this ONS calculator to calculate your own average life expectancy and probability of living until 100.

Historical Life Expectancy Trend

In fact, Yuval Noah Harari writes about Homo Sapiens becoming amortal, in his book Home Deus (Affiliate Link). With exception to someone being murdered for example, a person can continue to live forever. This is due to all diseases and even ageing being eradicated. This seems insane, but a little less when you consider the historical life expectancy trends.

In fact, this is no longer speculative. There is a branch of science known as senolytics that could produce a pill to stave of the health problems of old age, in a little as five to 12 years. This could spell the end of the aging process.

In England and Wales the life expectancy back in the 1700s was around 37 years of age. This didn’t change much over the next century and a half, even dropping to 25 prior to 1750. However 1850 seems to be the start of an explosive trend upwards towards a life expectancy of 80-85 years of age in the year 2000.

Across the world, life expectancy has increased, with the global life expectancy in 1800 being 22 years of age. As of 2012 the global life expectancy had increased to 70 years of age. That’s an increase of 48 years in just over two centuries. Even taking into account countries such as Sierra Leone pulling down the average. Although even the life expectancy there has doubled.

Future Lifestyle Design

Taking into consideration this life expectancy data and the fact you may live to 100. Forward retirement planning is crucial, as this money may need to last 35 or 45+ years, depending on when you retire.

Do you want to struggle or have to work for this lengthy period of time? Alternatively, you can invest early and increase your likelihood of being able to live the lifestyle you want for a prolonged period of time.

This growing life expectancy is one reason I previously wrote about why Financial Independence is a worthy goal, regardless of how long it takes.

I believe it’s critical to design the lifestyle you want when you retire, so that you can predict how much money you will need to fund this lifestyle. We will come to this calculation in a moment. However, if you would like some rough figures now, you can check out the infographic below from which.co.uk.

Forced Retirement

I have known family friends and most recently family, who expected to cover the gap in retirement savings by working on past the age of 65. Only for this bubble to be popped by mandatory retirement, with only a small financial compensation from their employer.

According to a survey by the Employee Benefit Research Institute,43% of workers end up retiring earlier than expected. However, only one-third say they did so because they could afford it. The most common reason for forced retirement were health issues, or the company making changes such as downsizing or reorganisation.

Another report by the Center for Retirement Research indicated that 37% of retirees had to stop working for similar reasons including; health issues, being forced to change jobs and retire when the new position doesn’t work out or pay as much, being laid off or the business closing. Familiar issues such as the need to care for a parent, spouse, child or grandchild also led people into unplanned retirement.

How Much Do You Need To Save

If you want to create a high probability that your money will last you through retirement, there are some simple calculations you can run.

- Calculate 25x your annual expenditure (e.g. £1500 (monthly spend) x 12 (months) x 25 = £450,000.

- Calculate your much you need to save and invest in terms of a lump sum and monthly contributions to get to this number using a compound interest calculator.

- Alternatively calculate what figure is realistically achievable for you.

- You can also use the awesome calculator below, from the The Wealthy Finn to calculate when you can retire.

I would also recomend you give The Wealthy Finn a follow on twitter by clicking here.

How To Make Your Money Last

Once you have calculated the above number. You can then calculate how much you can withdraw, in order to have a high probability of your portfolio never being depleted. In retirement planning, this is known as the 4% rule.

This simple calculation is as followers:

- Calculate 4% of the number that you calculated in the section above. For example, 4% of £450,000 = £18,000 per year. You can divide this by 12 to get a monthly allowance = £1,500.

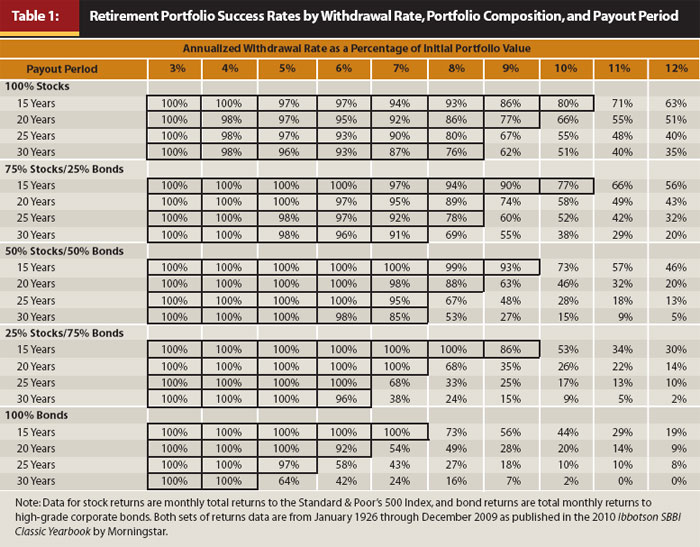

Research has demonstrated a 100% portfolio success rate when withdrawing at a rate of 4%. This outcome covered a number of portfolio compositions from 100% stocks to 100% bonds. Only dropping to as low as a 98% success rate for 75% stocks and 25% bonds over a 20+ year period.

However, certain ratios of stocks to bonds were shown to allow for a higher withdrawal rate. For example, a portfolio with 75 percent stocks and 25 percent bonds successfully supported a 30-year retirement with a 7 percent withdrawal rate through 91 percent of the sample overlapping periods.

Final Thoughts On Preparing To Live To Be 100

Investing in the stock market can be difficult, there are many intellectual and emotional barriers. If you want to get started and don’t know how, you can read my articleWhere To Start In The Scary World Of Investing: Simple First Steps To Get Started.

Maybe you feel that you do not have enough money to get started with investing. In which case you can read the following:5 Reasons Anyone Can Invest With Less Than £100.

On the other hand, perhaps you are already investing and want to save more, without feeling the pinch. In which case I would recommend one of my most popular articles Genuine Ways To Save Money Without Suffering!

Regardless of your position I would love to hear your thoughts on this article? Do you think you will live to be 100? Are you planning financially for this situation, just in case you do? Let me know your thoughts in the comments.

Trackbacks/Pingbacks